Hi! Lindsey here! I’m so excited to have a guest essay today from my friend Rebecca Gale! Rebecca is an award-winning journalist and staff writer at the Better Life Lab at New America. She also writes the newsletter It Doesn't Have to Be This Hard, where she examines why accessing child care is so challenging in the U.S. Today’s essay was born out of an email exchange Rebecca and I had earlier this year. Better Life Lab hosted a child care summit, and one of the speakers they invited couldn’t attend because they couldn’t afford the cost of the child care they needed if they were going to travel to the event. Oh, the irony! Ahead, Rebecca explores just why child care isn’t a business expense even if parents need it in order to work.

Every January, I receive a pile of 1099 forms tallying all the untaxed payments I received working as a writer with multiple bylines (including a Substack!). Inevitably, I owe the lovely IRS payment for the income I’ve collected as the hardworking journalist that I am.

One of the silver linings to freelancing is being able to deduct expenses that I incur with work. New laptop? Yep, that’s a tax deduction. The class I took on how to be a better data journalist? I can also deduct that as a learning expense. Mileage to and from the airport in my own car? Deductible at 70 cents per mile. Meals eaten while I’m out on assignment, or the latte I order while I’m writing this story up in a coffee shop? Also deductible, at half the cost.

But you know what is not deductible at all and is absolutely necessary for me to do work—arguably just as necessary as that laptop and definitely more necessary than that latte? Child care. And you know what’s not a deductible business expense? That’s right: child care.

In the U.S., if you’re traveling for work, and you need a babysitter to pick up your kiddos from school or get them ready in the morning, it can’t be considered a deduction connected to work.

But how can you do all the worky-work things you need to do if you can’t afford to pay someone to watch your kid? And why does our tax code accept first-class plane tickets, swank hotel rooms, and dining out to be reasonable business expenses but not the money spent hiring a babysitter or paying for after-school care so you can actually take that flight, sleep in the hotel, and go to the work dinner?

Part of this has to do with a provision tucked into the Child Care and Development Block Grants, which prohibits a parent from being able to collect compensation for caring for their own child. But another reason is that child care is viewed as a personal expense, not a business one. And our country’s tax system is largely set up in a way that prioritizes business expenses that drive up the country’s gross domestic product. Those personal expenses, our country’s law has concluded, are for the home front to handle.

By framing child care as “personal,” we, as a nation, are entirely off the hook for investing in the infrastructure necessary to support it. This is part of the reason why we have a fractured child care system: Parents are paying exorbitant amounts of money for care, child care providers working full time are making so little they must rely on public benefits to feed their own families, and many parts of the country do not even have enough quality child care options available for those who need them.

There is some good news: People are trying to change the thinking on this. The Federal Election Commission now allows candidates to use campaign funds to pay for child care needs that arise as a direct result of campaign activities. This means a parent running for office can use the campaign coffers to cover the cost of a babysitter while they are out on the campaign trail. Vote Mama, a group that tracks how campaign funds for child care are spent, found that the increase in spending on child care is particularly salient among those who have historically been underrepresented in elected office, and a majority of the funds spent by women candidates on caregiving services were by women of color.

As for me, I’d posit that leaving child care off the list of possible deductible business expenses is one more way that the tax code is designed for a non-parenting demographic. Which is particularly frustrating since the tax code is one of the only ways we provide parents financial support for raising children. The Child Tax Credit is one of the few family-friendly tax credits available for parents raising children. And in this last round of changes to our country’s social safety net, we made it out of reach for more families, including those whose kids would qualify but whose parents are not citizens.1

Many of us remember the refundable, advanced child tax credit of 2021: Those checks helped offset the costs of raising children in an emergency pandemic. But the impact of the cash was so significant that it cut our child poverty rate in half.

As I write this, we’re existing in this weird meta-phase with child care policy where the same administration that wants to cut food stamps and health care subsidies—essential for millions of American families—also purports to want to make a change surrounding child care costs, specifically those that can be addressed through the tax code. While adding child care as a business expense isn’t in any current legislation out there, that doesn’t mean it’s off the table entirely. If the FEC could make a change, perhaps there is a future where we see a change in the broader tax code, as well.

It’s frustrating that child care is so burdensome in the U.S., but it doesn’t have to be this way.

Now I’m off to drink my tax-deductible pumpkin spice latte, because that’s really what our country should be subsidizing, right? Or so our legislature would seem to agree.

-Rebecca Gale

Child care in the news

- Advocacy group Child Care Aware released its annual affordability survey in May and found that the national average price of child care for 2024 was $13,128. And prices have been rising exponentially. Between 2020 and 2024, the cost of child care in the U.S. has risen 29%.

- The Economist has an interesting look at New Mexico’s new free child care program, and how the state is attempting to attract new child care workers. And Marketplace spotlighted how one care center there is adapting to the policy.

- Part of New York City Mayor-elect Zohran Mamdani’s platform is to provide free child care starting at six weeks. What would it take to make it reality?

- Though families are saying they need more support when it comes to child care, many states are actually cutting programs. That’s due to Covid-era funding running out, as well as cuts to Medicaid included in the Big Beautiful Bill.

- Sara Mauskopf, founder and CEO of Winne, a child care startup, is one of Lindsey’s favorite voices in the industry. In a recent LinkedIn post, she wrote about why child care providers need more price transparency.

- If you’re looking for a true deep dive on the topic, Elliot Haspel, a colleague of Rebecca’s at New America, wrote the book Raising a Nation: 10 Reasons Every American Has a Stake in Child Care For All. This interview with Haspel in The 74 is also a good read.

What else we’re talking about

- I can’t get over the fact that the Brick, a physical device that can block your phone so you aren’t as distracted, is FSA/HSA eligible. Interesting times. (Lindsey wants to know if it works or if it’s a scam??) -Alicia

- Wonderland Books in Bethesda, Maryland, hosted author this week to speak about her new book, Wreck, which I can’t wait to read. I was so impressed with Newman’s outfit of a silk shirt tucked into Adidas track pants with boots. I definitely want to recreate this look. -Rebecca

- I wrote about how logging off can help your finances. -Alicia

- The winter holidays are not my favorite time of year, and I turn into something of a Grinch from the day after my birthday until January 1 because I just get so overwhelmed by it all. I absolutely loved this piece from about how her husband took over the gift-buying responsibilities last year. -Lindsey

On our radar

I’m getting on a plane to Vermont to report out a long-form story about how this small-but-mighty state passed the nation’s first near-universal child care plan. Hard things can be done, people. The only thing freaking me out is the fact that it’s snowing there. -Rebecca

I’ve known Stash Wealth founder and CEO Priya Malani for close to a decade now, and she’s one of my favorite people to talk to about money and life. Naturally, the conversation just flowed when I joined her recently on her podcast, The F Word. -Lindsey

Don’t forget we’re having a birthday sale this month! Annual subscriptions are just $45.60 (down from $80), and we’re donating $5 of every new annual subscription to a food bank.

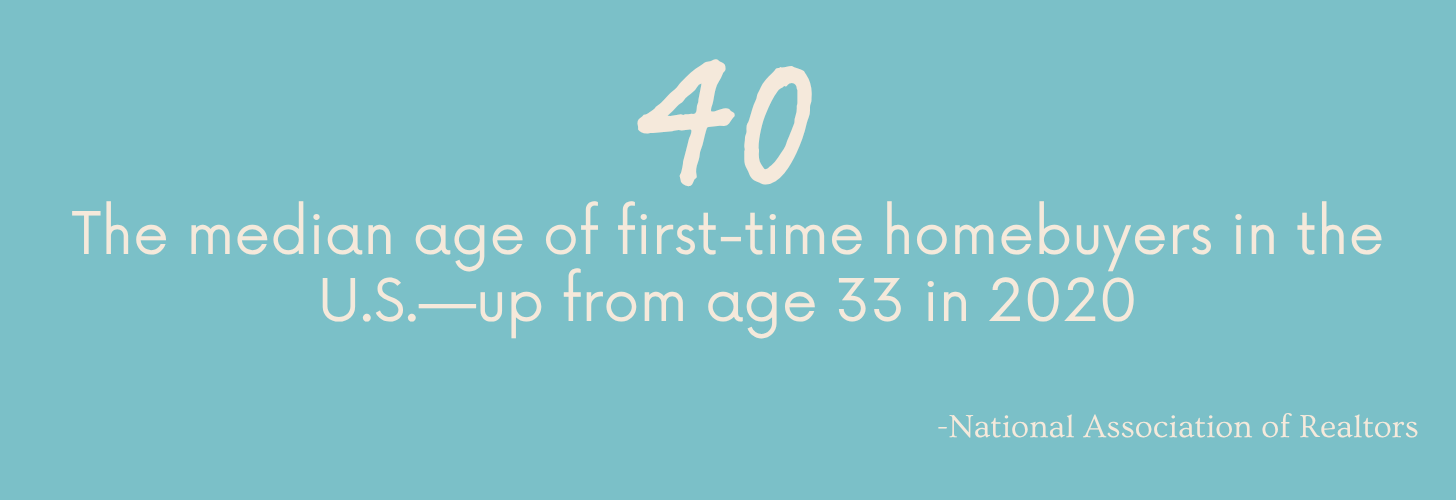

Stat of the week

Best money we spent last week

- I didn’t spend any money outside of groceries this week, but I did get refunded $260 after emailing the company about a weird subscription renewal, so here’s my reminder to always ask! -Alicia

- I actually had a Purse-themed purchase: a new pair of sheer black tights after a good friend informed me I need to be wearing sheer for nighttime events and not opaque. Hoping this one thing elevates an entire outfit. $44 -Rebecca

- My kid and I spent hours at the allergist on Tuesday, which was no fun for either of us, but especially sad for Freddy because it was a day off from school, and who wants to spend a day off waiting around for an allergen poke test? He was so patient that I promised him a reward. This might be the first time I haven’t been grumpy about buying Robux! $20 -Lindsey

The other major tax assist for child care costs is the Child and Dependent Care Tax Credit, which allows parents to take a tax credit toward the costs of licensed child care. This credit though, in the words of one economist I spoke to, is not considered a “big deal” for balancing the IRS checkbook because so few families take advantage of it, and almost all that do are middle to high income, since the credit is not refundable for people with a lower tax burden (the credit cannot exceed a family’s tax bill). ↩