When you’re in your twenties or even thirties and just starting off on your financial journey, figuring out how to earn, save, and spend your money in the moment will feel all-consuming. There’s always another budgeting app to try, goal to strive for, and bill to pay.

But according to a seasoned financial professional, 20-somethings shouldn’t just be living for the here and now—they should be paying much more attention to how they’ll be living in 40 years.

“We’re finding that our younger working adults are living for today and not necessarily for their retirement,” says Jessica Nino, a certified financial planner with Edward Jones. “We're seeing a lot more, ‘I’ll worry about retirement later. I’m just going to use my extra money to buy this new car.’ Versus taking those long-term goals more seriously.”

It’s not so surprising that people might want to spend more to make life a little more tolerable now, when daily stresses compound and the economic outlook is bleak. Throw in the threat of foreign wars, AI’s evolution, and climate change, and it can be hard to even imagine a future 40 years from now.

But the time will pass—and you don’t want your future self to be left with nothing. Plenty of people say their biggest regret in retirement is not saving more; few, if any, say they saved too much.

“[Young people are] just not wrapping their brain around, ‘Hey, I’m going to be 65 someday and need to think about retirement,’” says Nino.

How much to save

What does it mean to be serious about saving for retirement? For 20-somethings (and even 30-somethings) early in their careers, it means making it a priority to set aside at least some money each month in a tax-advantaged retirement account.

Exactly how much to set aside will depend on your personal circumstances. But generally, an overall savings rate of 10 to 15% is advised by most financial experts. And while putting money aside in a savings account is great, investing in a tax-advantaged account like a 401(k) or IRA can help your money grow and compound.

If you are offered a retirement plan at work, that’s the best place to start. Often, employers that offer a 401(k) or similar plan also offer matching contributions, such as a dollar-for-dollar match up to a certain percentage of your income (typically 3% to 6%). Contribute enough to at least receive the full match—otherwise, you’re effectively taking a pay cut. Beth Kobliner, personal finance expert and author of Get a Financial Life: Personal Finance in Your Twenties and Thirties, explains:

Let’s say your company matches 50 cents for every dollar you contribute to your 401(k), up to 5% of your salary. So if you make $50,000 a year, you should put in $2,500 to get an employer match of $1,250. Contributing any less is like walking away from free money.

If you don’t have access to a workplace retirement plan or simply want to save a little more, most advisors suggest young people look into Roth IRAs. When you contribute to a Roth IRA, as opposed to a traditional IRA, you invest money that you’ve already been taxed on. When you make a withdrawal in retirement (after age 59 ½), you don’t pay tax on the earnings.

Those tax benefits make a Roth IRA a particularly attractive savings opportunity for young people who are likely in lower tax brackets now than they will be later in life—you pre-pay taxes at your lower rate, and then don’t have to worry about them again.

Time in the market

As financial experts will tell you, the importance of starting to think about retirement when you’re young because of the time value of money. How long you have your money invested is often much more important than how much you invest.

More time in the market gives your investments more opportunity to compound, where your money is earning interest on top of interest.

And those retirement accounts mentioned above have another advantage: Taxes are generally deferred until you make withdrawals, which is not the case with a taxable brokerage account. While that may not sound like a big deal, the result is thousands of more dollars over a lifetime, Kobliner explains.

“When this happens for, say, 40 years rather than 30, it not only grows for a longer period but also grows more quickly,” she writes.

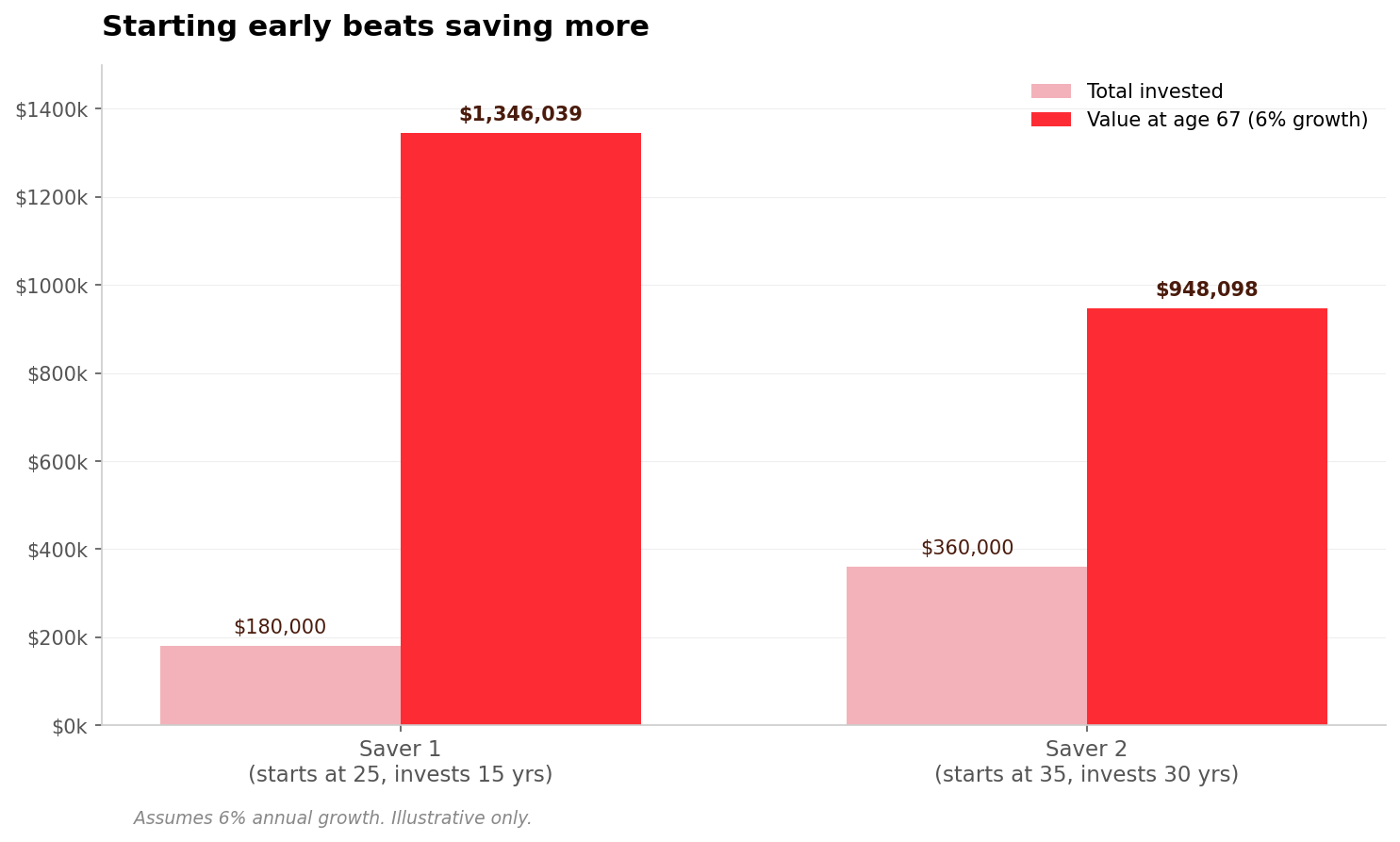

Take the following example from Principal Financial. Assuming annual growth of 6% (which is actually relatively conservative), someone who invests $12,000 per year from age 25 to 40

will have far more money by the time they reach retirement than someone who starts 10 years later—even if the 35-year-old invests $12,000 per year for the next 30 years. It’s almost impossible to make up for that early compounding.

Though past performance doesn't guarantee future results, investing in low-cost index funds or ETFs (what more retirement accounts offer) has historically shown substantial growth over the long term. Try playing around with a compound interest calculator to see the full effect.