This post is sponsored by Get a Financial Life: Personal Finance in Your Twenties and Thirties.

When Beth Kobliner first published Get a Financial Life: Personal Finance in Your Twenties and Thirties in 1996, the median home cost $140,000, the first budgeting app wouldn’t launch for another decade, and index fund investing was not yet the go-to wealth-building strategy it is today.

A lot has changed since then. And yet so much sound personal finance advice from the time still holds true. Kobliner’s book, too, stands the test of time. Now updated to reflect all of the latest research, financial product advancements, and legislative changes of 2026, Get a Financial Life is still a must-read for anyone starting their first job—or simply starting to take their finances a little more seriously.

In easy-to-follow chapters, Kobliner guides you through the big personal finance questions including: how much you can reasonably save, how to choose the right credit card, which student loan repayment plan to pick, and how much house you can actually afford. She breaks down complex financial jargon while focusing on what the average reader actually needs to know and gives simple, actionable advice throughout to help you level up your finances.

Here are four of the takeaways for 20- and 30-somethings from Get a Financial Life.

Get more serious about saving

Once you get a handle on your income, basic expenses, and any debt you may have, one of the most important financial habits you can start to form when you’re young is saving. Regardless of what your short- and long-term dreams are—buying a house, pursuing a passion project, having a kid or two—you’ll need money to fund them.

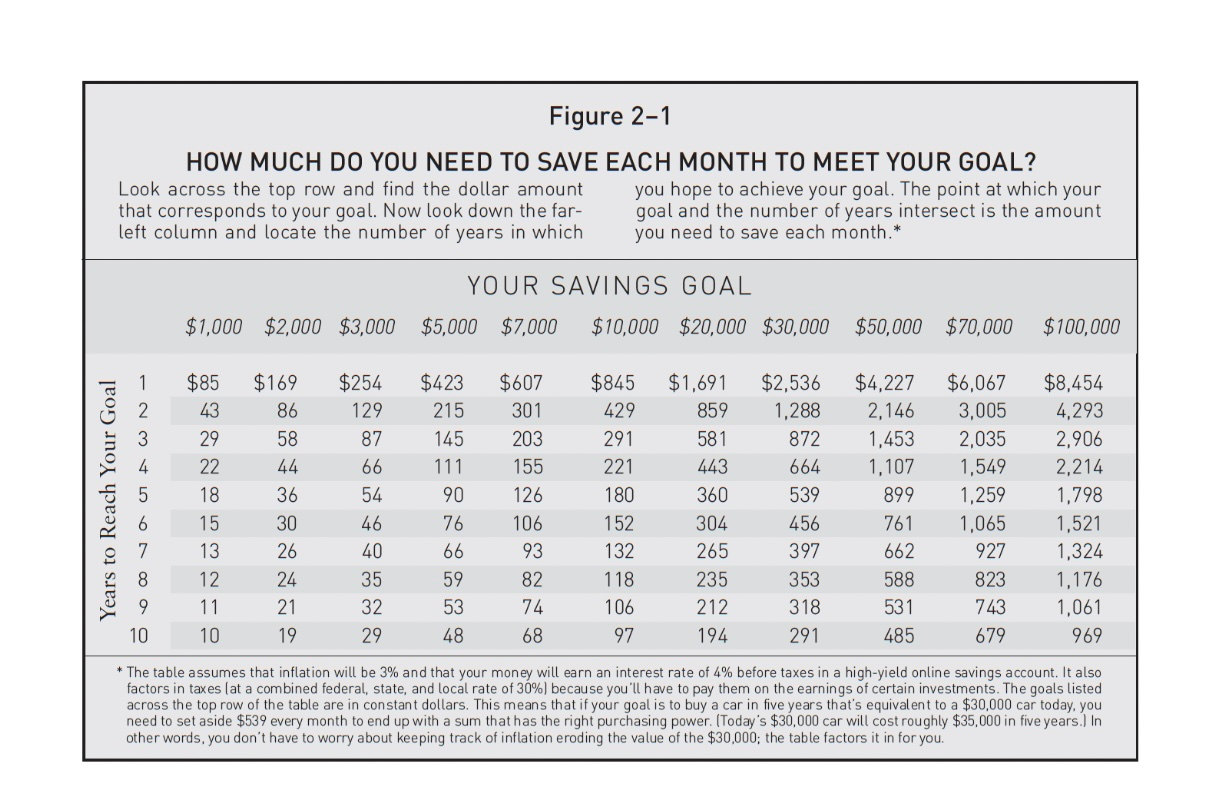

And as Kobliner writes, “the first step toward turning your financial desires into achievable goals is calculating the dollar value of your dreams.”

To that end, Get a Financial Life provides a simple chart I liked so much I actually printed out and taped above my desk. It gives you a rough idea of how much you need to set aside each month to end up at a specific dollar amount after a set number of years, assuming there’s 3% inflation and you’re saving money in a high-yield savings account (HYSA) with a 4% APY.

(Speaking of a HYSA, Kobliner also gets into the importance of having one and why online banks often have better options than traditional brick-and-mortar banks.)

In order to save, you’ll need to know where you can cut spending. One way to do this, Kobliner writes, is to keep a spending diary for a week. You can do this using a dedicated budgeting app app, on a spreadsheet, or even just in your Notes app. You can also see if your bank or credit card provides a spending analysis tool that organizes all of your charges into different categories to give you a holistic overview of your finances. (I bank with Capital One and was recently offered this tool.)

When reviewing how much you’re spending and how you have left over each month, ask: Can you save 15% of your pretax pay each month? This is a rough financial rule of thumb Kobliner recommends aiming for, at least when you’re starting to save.

“While there’s no magical reason to save exactly 15%, it’s a good target to aim for,” she writes. “Include in that 15% the money you set aside to meet your short-term goals as well as the money you put in a retirement plan.”

Prioritize paying off your high-interest debt

If you have any sort of high-interest debt (like on a credit card), it’s almost always going to be better to put your savings toward paying it off than hold on to more cash than you absolutely need.

“The interest rates on such debt are higher than the interest rates you can expect to receive from investments,” Kobliner explains.

“In most cases, the very best investment you can make is to pay off your credit cards, private student loans, and auto loans,” Kobliner writes. “Paying off a credit card balance with a 20% interest rate, for instance, is in effect paying yourself 20% interest, guaranteed and tax-free. That’s a great return.”

Of course, personal finance is personal, so there’s no one-size-fits-all rule you absolutely have to follow. If having no or very little savings will cause a lot of anxiety and mental anguish, then keep a little cash set aside. But try to pay off as much debt as you can when you can as fast as you can.

Consider inflation (but don’t overthink it)

Related to the above, Kobliner makes an interesting point I haven’t seen explicitly laid out elsewhere: It’s important to have a savings (and investing) goal, yes; but it’s also important to remember the purchasing power of your money.

“It’s easy to forget the effects of inflation when you think about how your money will grow over the years,” she writes. “Say your parents bought a new car for $16,000 in 1993. If you bought a comparable car today, you’d pay about $48,000. Put another way: $16,000 today buys only about a third of the car it bought in the 1990s. Terrifying.”

So when you’re thinking about a really far off goal like retirement, you will need to save a little more than you’re thinking about now. Inflation will continue to grow in the years to come, and what a comfortable retirement looks like today will look different in 40 years.

Likewise, for those just starting to save for a home, prices might be much different in, say, 10 years than they are today. (Just look at the difference in prices between 2016 and today.)

That’s why it makes sense to invest some of your money in stocks and bonds rather than just keeping it all in a HYSA. They are a little riskier than a savings account, but they can help you fight back against inflation when you’re trying to save for long-term goals.

“Inflation can drastically reduce the purchasing power of the dollar over time,” Kobliner writes. “This doesn’t mean you shouldn't save…you still come out way ahead if you start saving in a retirement account while you’re young.”

Start investing now

Speaking of retirement, the earlier you begin investing for that distant future, the better.

This is one of those things you’ve probably read a bunch of times but may not have truly taken to heart. You can always catch up on your savings later when you’re earning a little more, right?

As Kobliner’s book lays out, it’s a lot easier to build wealth if you start younger:

“Suppose you set aside $1,000 a year (about $19 a week) from age 25 to age 65, a total investment of $40,000, in a retirement account earning an average of 7% a year. By the time you turn 65, you’ll have $213,610.

“But if you don’t start saving until you’re 35 and then invest $1,000 a year for the next 30 years, a total investment of $30,000, you’ll have only $101,073 when you turn 65.”

And it’s important to do this in a tax-advantaged retirement account, like a 401(k) or individual retirement account (IRA). When you contribute to these specific accounts, the government does not tax the money in the account while it’s accumulating interest and other earnings. That’s what makes them, in part, such great investment tools.

In fact, if you take one thing away from this entire article, I hope it’s this: Contribute what you can to your retirement account as early as you can. It is extremely unlikely there will ever come a time when you wish you would have saved less for the future, but plenty of people regret not having enough saved. You might as well get a jumpstart now.

The most frequent comment Kobliner says she’s received from readers of her book is how happy they were that they opened a retirement account in their 20s, even if it felt like they couldn’t really afford the contributions in the beginning.

“Once they bit the bullet and had money from their paycheck automatically siphoned into a tax-favored retirement plan, they often say they were surprised how quickly they adjusted their everyday spending,” she writes. “Before long, they hardly missed the extra cash.”

Check out chapter 6, “Living the good life in 2075” for more information on the difference between retirement accounts and how to choose the best one for your financial situation.

Pick up your copy of Get a Financial Life: Personal Finance in Your Twenties and Thirties for more financial advice from Beth Kobliner.