The one year anniversary of Liberation Day is Thursday, and though it’s not much of an auspicious anniversary, it does drive home the importance of following one of The Purse’s Principles of Personal Finance*: When the market starts tanking, it’s best to leave your money alone.

If you don’t remember the grand event, Liberation Day was what the Trump administration deemed their unveiling of tariffs unilaterally imposed on virtually every country on Earth. It arguably didn’t go so great. While the president was still unveiling the new levies, stocks cratered, experts thought the U.S. dollar might lose its status as the world’s reserve currency, and even Treasuries didn’t look safe as investors started to lose faith that the United States would uphold its promises and obligations.

Truthfully, we’ve had many scary moments over the past six years. And those, to me, are extremely edifying when it comes to managing your finances and investments.

Take the Covid-19-induced shock to the stock market: at its lowest point, the S&P 500 lost about one-third of its value. It’s easy enough to read the advice not to make any emotional financial moves when major news events like that happen, and much harder to actually not do anything when it happens in reality. Something like a worldwide pandemic must surely mean things are different this time, right?

Wrong. Stocks fell precipitously in March 2020 before recovering completely by August, just five months later. And in the six years since they have since taken off at a pace never before seen in world history even with the occasional dip.

In fact, financial research from firms like JPMorgan has shown that missing just a select few of the market’s “best” days has an outsized impact on your finances, and these days tend to come shortly after a market drop. If you pulled out investments or stopped contributing when things got choppy, you will likely lose out on the most significant gains. Seven of the market’s 10 best days occurred within two weeks of the 10 worst days, according to JPMorgan.

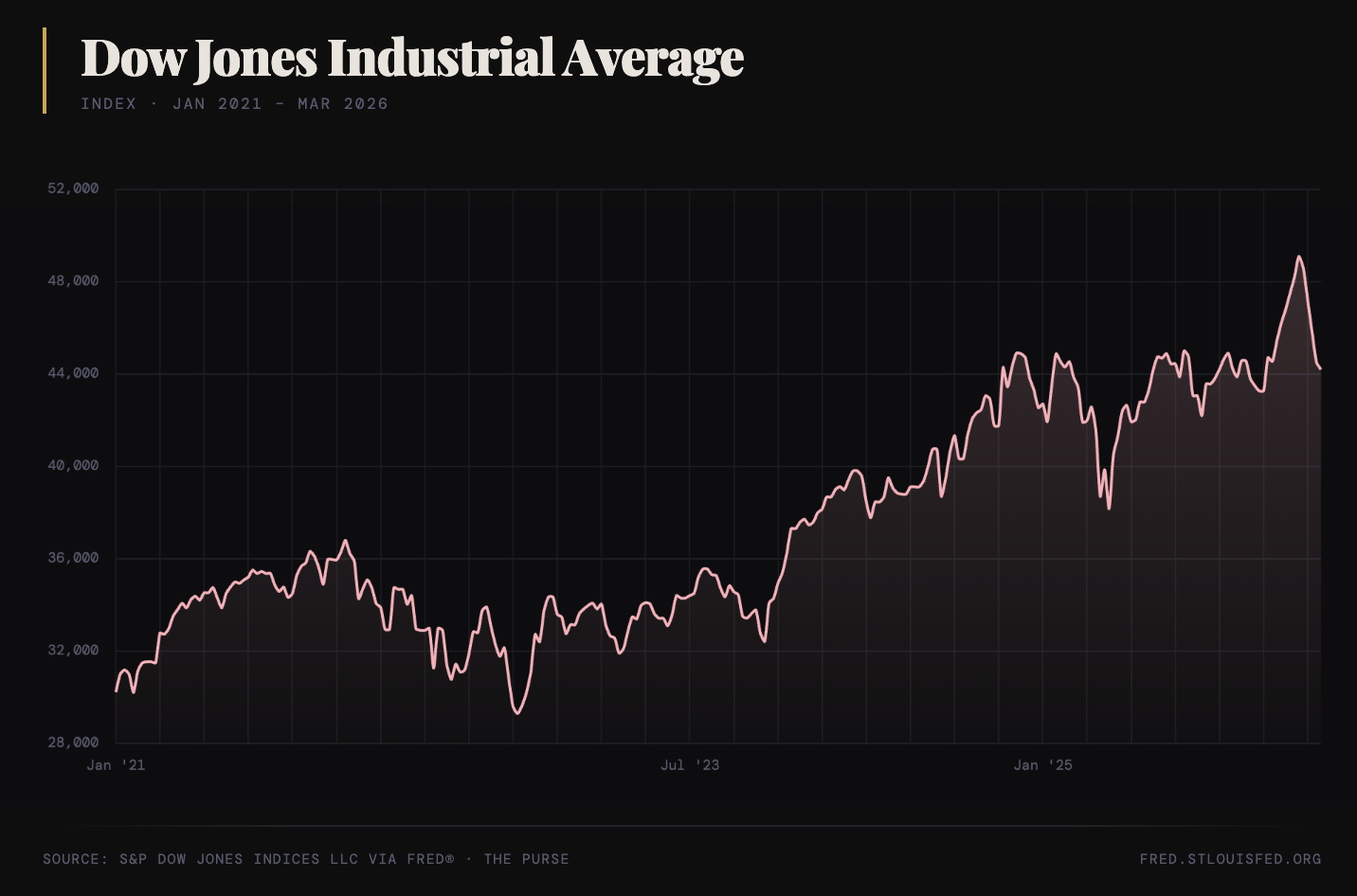

When Trump announced his illegal tariffs last year, it truly seemed like the world economic system was going to melt down.

Yet the advice from the many financial advisors I spoke to at the time remained the same: Don’t do anything. Wait it out. My editor at the time questioned the story and their advice. Surely, she said, this time must be different?

At least so far, the financial advisors were right again. Stocks rebounded and hit new highs; the economy somehow keeps chugging along. If you had pulled out of your investments following the Liberation Day drama, you might feel a little silly now.

This new war, and especially the effects it is having on the global oil supply, is presenting new, painful problems. But while the stock market has been rocky—with a few indexes closing in correction territory in recent days—we haven’t seen anything near the Covid or Liberation Day jolts to the system yet.

And the reality is that there will be another bear market, another recession, another financial calamity—it’s only a matter of time. That’s why it’s so important to have a financial plan that reflects your risk tolerance. If recent market nose dives made you uneasy, then it’s imperative to prepare before the next economic pain point.

For me personally, this means having a little more cash on hand than some experts might advise. I like knowing I have a cushion, and that I wouldn’t need to tap into anything for many months if I needed to. Building up my emergency fund has been my number-one priority since paying for my wedding and finding more stable income post-layoff.

The worst time to make changes to your financial plan is in moments of uncertainty or extreme chaos. Let Liberation Day be a lesson.

Read more:

*We have yet to officially write down our Principles of Personal Finance, but you can expect it soon!