Hi! Before we jump into today’s edition of 30-something, just a reminder that we’re having a big sale on annual subscriptions right now for Lindsey’s birthday. Until November 30, you can get an annual subscription for $45.60 (usually it’s $80), and we’ll be donating $5 from every new annual subscription to a food bank.

Among my friends with student loan debt, a sort of malaise has set in. We’re now well into our 30s, a decade or more out of college, and many have given up hope they will ever fully pay their loans off. The debt is always just kind of lurking there, floating in the background, haunting us like a ghost of financial decisions past.

Americans owe around $1.64 trillion in student loan debt, according to the New York Federal Reserve, and student debt is the third-highest category of household debt in the U.S., behind mortgages and (just barely) auto loans. Many argue that it’s “good” debt, but it still has negative implications for those trying to pay off five- and six-figure balances. Generally, student loan borrowers have to delay home ownership and often save less for retirement when compared to their peers without college debt.

I’m one of the lucky ones. I don’t have student loan debt—I attended an “affordable” in-state college and was extremely fortunate that my parents were able to put aside enough to pay tuition and room-and-board costs for my sister and me. But I have reported on the topic for years, including closely following President Joe Biden’s blanket forgiveness efforts, which were subsequently overturned by the conservative-majority Supreme Court a few years ago. I’ve interviewed dozens of millennials about their experiences, and it’s hard to not feel despondent when you consider how this debt has negatively impacted their lives.

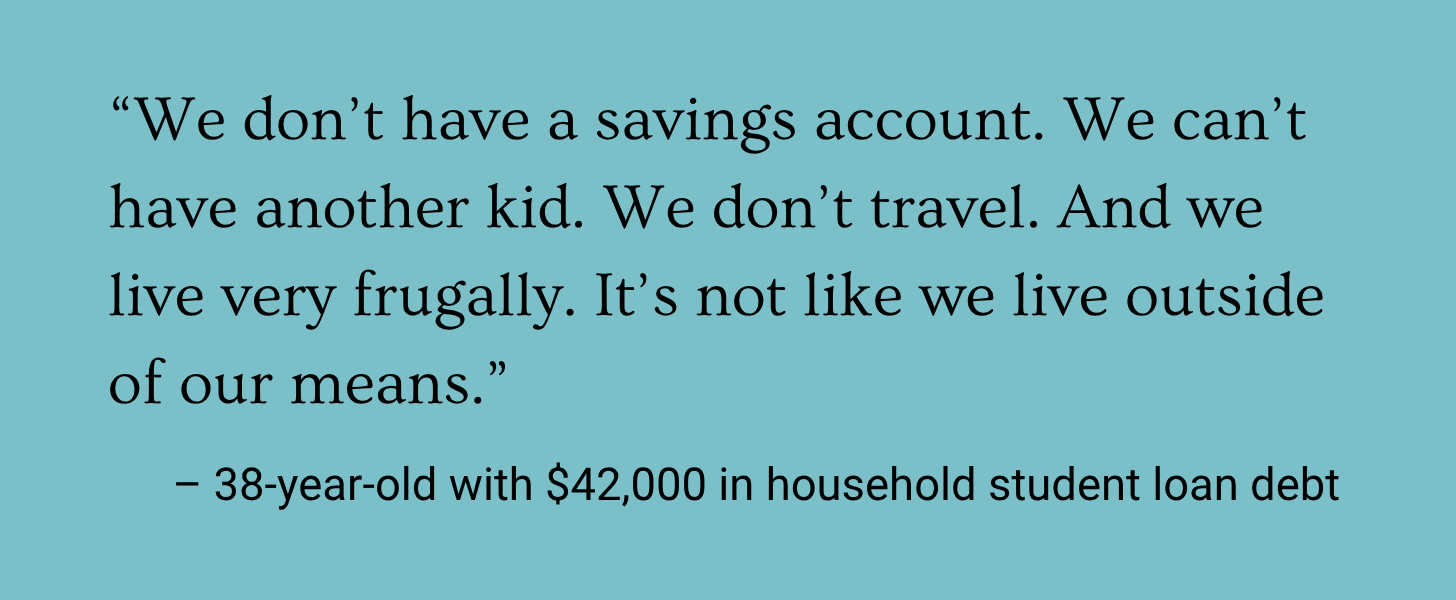

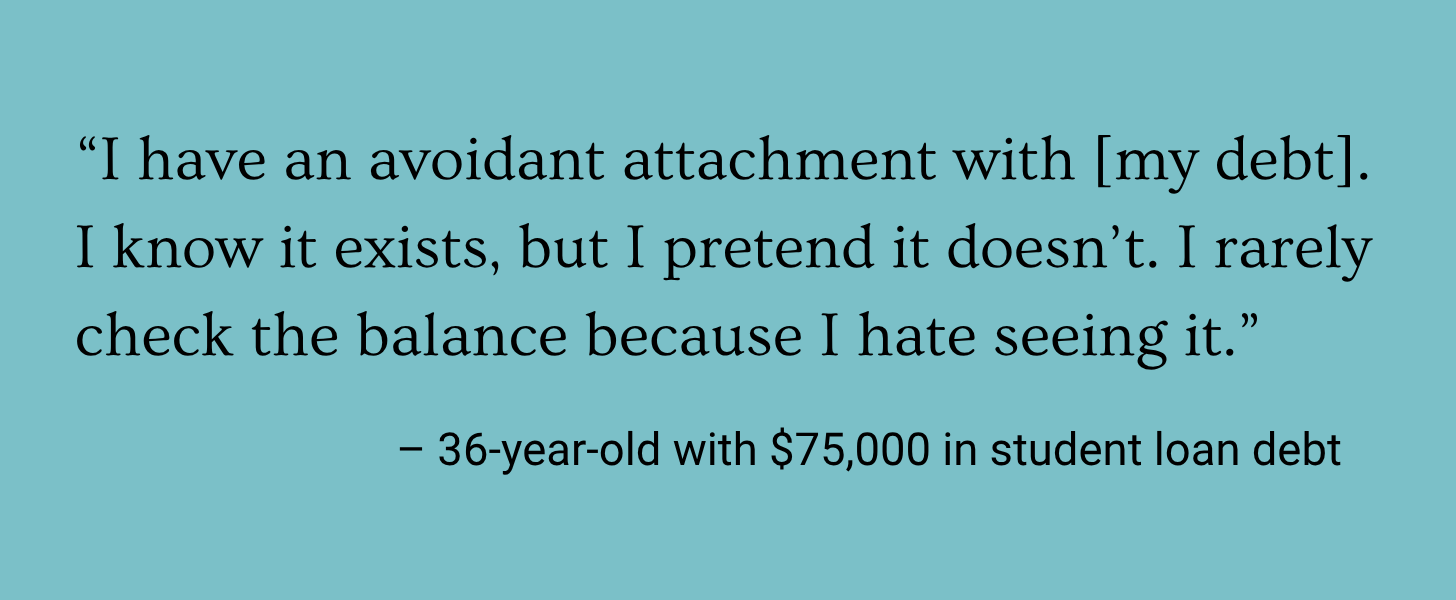

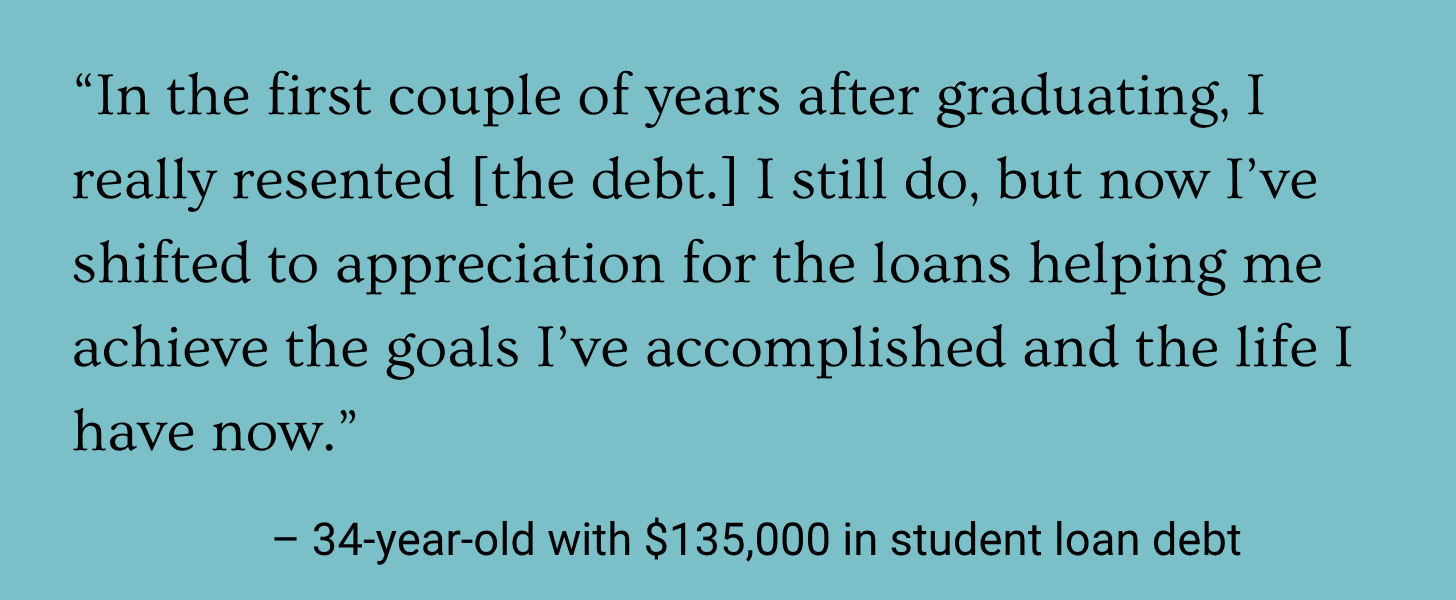

I don’t think you can write about being a 30-something in the U.S. and not discuss student loans. So recently, I asked 30-something readers of The Purse how their education debt is impacting their lives. Some wrote that it makes them feel “nervous” and “disheartened,” especially with the federal government constantly changing the rules around repayment and forgiveness programs. Of the 18 who filled out the questionnaire, virtually all had regrets, while acknowledging the loans were a “necessary evil.”

Beyond delaying important life milestones, carrying student loan debt also impacts how our generation is navigating their careers. My close friend just lost her high-paying tech job—one she took not because she loved the work, but because she wanted to focus on paying down her loans faster. Now she worries about rushing into yet another soul-sucking corporate role just to ensure she’s able to make her student loan payments on time.

A 36-year-old therapist with a $71,000 student loan balance wrote to The Purse that even though she loves her work, her loan burden has affected her relationship to her career, and sometimes she regrets that she pursued her degree. “Sadly, it makes me think that some professions only work for people with generational wealth or solid financial support from family,” she wrote. “Which is a shame in the mental health field, since we need diversity in clinicians.”

The responses echo feelings my friends have relayed over the years: Taking out student loans allowed many to pursue their dream careers, but the reality post-graduation hasn’t necessarily lived up to the promises. How unfair it is that it’s often 17- and 18-year-olds making the life-altering decision to take on this debt without fully understanding what it means to borrow so much money.

“I waiver from being extremely stressed to ignoring it and being in denial,” said a 38-year-old who attended medical school and pays over $2,000 a month in student loan debt. “There is a ton of guilt surrounding it for me, especially now that I have a family and child to provide for.”

The debt load is so heavy—mentally and financially—that almost all respondents said if they could go back, they’d opt to attend less expensive schools or search for better scholarships. They’d avoid private loans and double down on making interest payments while still in school.

But I was particularly struck by the anxiety permeating responses from those who have been trying to qualify for the Public Service Loan Forgiveness program, or PSLF. Under this program—which was created in 2007—those who work in qualifying public service jobs for at least 10 years and make 120 on-time payments can apply to have the remainder of their loan balances erased. It’s the government’s way of saying this work matters.

Now, thanks in part to the current presidential administration, the future of PSLF is uncertain, and borrowers who have staked their careers and financial futures on seeing their debt forgiven are left in limbo. One 31-year-old I interviewed is just a year away from qualifying for forgiveness but notes that the program is currently on pause due to ongoing litigation. The Trump administration also recently changed the rules around the type of employers that can qualify for the program.

A recent edition of Home Economics shows how life-changing loan forgiveness can be when it works as designed. A couple from Maryland had over $500,000 in loans forgiven. It gave them enough breathing room that one spouse was able to take a lower-paying but more flexible job and still save for their disabled daughter’s future.

Millions of borrowers planned their careers around receiving PSLF; how could they have reasonably predicted the government could change the rules on a political whim? To think that this benefit might disappear after so many young people dedicated their lives to public service feels unconscionable. “I’m nervous that I will have spent a decade in an underpaying job just to have the rug pulled out from under me,” the 31-year-old said.

For years, we heard the constant drumbeat of the necessity of a college degree to get ahead—or get anywhere. Fast forward to today, and politicians and op-ed writers across the country have now decided that the real problem is all of those silly millennials who really should have known better before taking on all that debt just to get their college diplomas. Rather than trying to fix the systemic problem, we simply blame others for their financial challenges.

Student loan debt has become one more cudgel used by politicians to divide voters, another us-versus-them line of attack that makes little sense. Ultimately, millennials’ unmanageable student loan burden is yet another economic disappointment in a long list that has a wide-ranging impact on this generation. But if you’re one of the 43 million Americans with student loan debt, it feels deeply personal.

“It is always lurking in the background affecting all my decisions,” said a 36-year-old with $300,000 in student loan debt, including from law school. “It scares me to buy a house, get married, change jobs because my student loans could be affected.”

How have student loans impacted your life? It’s worth noting that it’s not just millennials who are struggling with the burden of student loans. The Wall Street Journal reported in September that “[t]he six million-plus borrowers aged 50 to 61 have the highest average balance of any age group, at $47,857, according to Federal Student Aid data.”