A big thank-you to our sponsor Acorns Early, a banking app for families! Right now, we’re offering a special deal: Get a free one-year annual subscription to The Purse when you sign up for an Acorns Early account.

A common theme I see pop up again and again in my work is that people often feel they didn’t get an adequate financial education during their childhood. Most of our parents didn’t talk to us about money while we were growing up, and as a result, many of us don’t feel equipped to manage our own finances as adults. And now that we’re parents, we’re trying to break the cycle.

But it’s hard! Kids ask tough questions! And there’s not really a clear playbook to navigate this tricky topic. How can you teach your kids to be smart with their money while avoiding passing on your own baggage?

I don’t have all the answers, and I’m learning alongside you, dear readers. The tough kids-and-money topic I’ve been wrangling with for a while now is allowance. This spring, after I finally gave in and let my kid, Freddy, get a Roblox account, I realized that an allowance might be necessary so he’s not constantly asking us for more Robux. (For the uninitiated, “Robux” is the in-game currency for Roblox, and it costs real money. You won’t be surprised to hear that if you’re not careful, those purchases can add up quickly.)

So when Acorns Early approached me about working together, I jumped at the opportunity. Here was a chance to get my butt in gear and set up an allowance for Freddy, who’s eight. And I knew he’d like the gamification element of the Acorns Early app, where he can see his money on his tablet app, as well as play financial literacy games. It felt like a win-win.

Acorns Early (formerly GoHenry) is for kids ages 6–18. It’s a great way for them to learn the value of money. Acorns Early helps kids develop healthy earning, saving, budgeting, and spending habits that will last a lifetime.

But there are a few things I had to decide before I got started. I’m sharing my thought process ahead in hopes that it might help you if/when you decide to start giving your kid an allowance.

So where to begin? I found it helpful to ask myself the following questions.

1. Is the allowance tied to chores?

Most people agree that giving an allowance isn’t a bad idea, but there is some disagreement over whether you should tie the cash to chores.

I’m of the camp who believes that kids shouldn’t get an allowance for helping out around the house. I don’t get paid to make the bed, and Ken doesn’t get paid to do the dishes. We do these things because we are good members of our household, and as our kid gets older, he should be helping out more, too.

With this in mind, I decided I wasn’t going to pay Freddy for the various things he has to do around the house, like taking out the compost and practicing piano. But I like that Acorns Early let me set up a list of to-dos for Freddy that he can check off as he finishes them. If he’s anything like his mom, he’ll appreciate the satisfaction of crossing tasks off a list.

Of course, there can still be consequences if your kids don’t do their chores. Maybe you limit screen time until the work is done, or you cancel a fun activity. Ken always talks about his childhood friend who could never come out to play until his room was clean.

I actually discovered a funny trick that works for Freddy that I call the “anti-allowance.” He had a really bad habit of leaving his food wrappers all over the living room. I told him I was going to start charging him a dollar for every wrapper I found. It’s worked surprisingly well!

Some families do find success in giving their kids an allowance for doing chores. It motivates them to help more, and they get satisfaction for being paid for a job well done. As reluctant as I am to go that route, I can see the benefits of monetarily rewarding your kids for their work. In the Acorns Early app, you can give each chore a monetary value—$0.50 to put your clothes away or $1 to take out the trash. I could see how tracking the money adding up each time you finish a task could be pretty motivating.

Ultimately, it comes down to what kind of kid you have. If your kid starts asking for an allowance, find out why they want one. What do they want to spend their money on? Understanding their motivation can help you know how best to move forward.

2. How much allowance?

Among my friends in Brooklyn, we are all aligned that the going rate for the tooth fairy is $5. But when it comes to allowance, we are not all on the same page.

When Ken and I started talking to Freddy about getting an allowance, I asked him how much he thought he should get. I had been thinking $5 a week sounded reasonable, so I was a bit taken aback when he suggested $10. That seemed like a lot to me, but as he pointed out, ice cream at a Mr. Softee costs $7. Fair point.

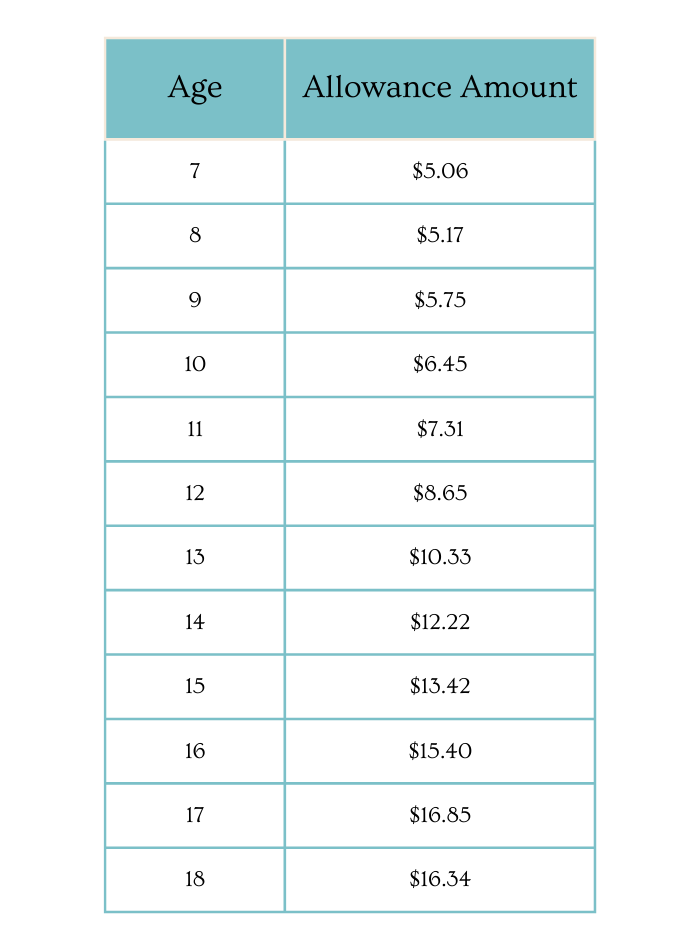

Acorns Early surveyed customers in 2021 to find the average weekly allowance by age:

While I thought $10 was a lot for an 8-year-old, I feel like $16 is sort of low for an 18-year-old. Of course, by 18, you can go out and get a job, which is not the case for younger kids. Minimum wage in New York City is $16 an hour, so even an hourly gig will be a better deal for most teens if they can find work.

I’ve also read that some experts suggest giving your kid $1 to $2 per week for each year of their age. If I followed that rule of thumb, my kid would be making $16 a week! Suddenly $10 seems very reasonable.

Ultimately, I decided to go somewhere in the middle and landed at $8 per week.

3. How much control do I have over how he spends the money?

One issue that comes up again and again with allowance is how kids should spend their money. Now that he’s earning $8 a week, what should he spend that money on? And how much of a say do I have over it? Usually, I don’t have a problem picking up the tab on treats like ice cream. But will I feel differently now that my kid has a steady income stream?

Experts recommend teaching your kids to split their allowance into separate buckets for saving, spending, and giving. In the Acorns Early app, you can easily bucket cash into each of these three categories. The app has teamed up with the Boys and Girls Club of America, so your child can automatically donate some of their allowance to that charity. But if they want to donate to a different cause, you’ll have to set that up separately.

A good rule of thumb is to set aside 10% for giving, 20% for savings, and 70% for spending. Establishing those metrics when you’re young can help you build good financial habits you’ll (hopefully!) keep for life.

With those guidelines in mind, I’m encouraging Freddy to donate $1 per week and save $2 per week; that leaves him $5 to spend as he pleases. Of course, I hope he doesn’t feel he needs to spend it all every week and starts to see the satisfaction you can get from letting your cash accumulate. Via the Acorns Early app, Freddy can set his own savings goal, choosing from one of the popular goals (sneakers, phone, gaming console) or creating his own.

When I agreed to let Freddy sign up for Roblox, I made a rule that he couldn’t spend more than $10 a month on Robux. But now that he has his own allowance, I’m taking back that rule. I won’t be spending any of my money on Robux, but I’m going to let him decide how he spends his own allowance. It’s hard, but I do believe you have to let your kid make some bad spending decisions from time to time so they can understand what it feels like to regret a purchase. We’ve all forked over cash for dumb things—a bad meal, an ill-fitting pair of jeans, or expensive shoes that pinch your toes (this can’t only be me!)—but making those mistakes when you’re young and the stakes are lower can help you learn so you don’t make them (as often) when you’re older.

4. What tools do you need?

As with many things related to raising kids, you can make this as simple or as complicated as you want! You can just give your kid cash each week and call it a day. Or you might decide to go the fintech route and choose an app like Acorns Early to help facilitate the process.

With the Acorns Early app, you can get the first month free, and then it’s $5 per month per kid. Families with up to four kids pay $10 per month. The app comes with a lot of bells and whistles that helps make money management easier for everyone involved. Beyond setting up regular allowance deposits into their account, the app gives your kid a debit card they can use to make purchases in stores. You can also invite grandparents and other relatives to transfer money to the account for birthday gifts and the like. And as kids get older and start hanging out more without parents, there’s a way for them to transfer money between friends.

The app also allows you to set spending limits and track how your kid is managing their money—and doing their chores. You can easily transfer money between accounts, which can be especially helpful if you’re out with your kids, and they want to buy something with cash. And ideally, both of you seeing everything in one place will help spark conversations about spending, saving, and giving. Which is the whole point of this allowance experiment, right? Right!

What else?

I think the most important thing with allowance is to make sure you actually give your kids the money you’ve promised them. Most of us don’t carry cash these days, and it’s easy for an allowance to quickly become something that’s theoretical with a whole lot of IOUs.

But for kids to really understand money, they need to see it—even if that means they’re looking at their savings growing in an app. (Which is probably better than our current system, where Freddy is accumulating his cash in his sock drawer.) It’s also important to talk about the cost of things in order for our kids to understand the value of a dollar.

Offering an allowance is just one step in helping kids understand money—and your family values. Don’t feel bad if you try it for a while but it doesn’t stick. The important thing is you’ve started the conversation.

Kids aged 6–18. © GoHenry Inc. ("Acorns Early"). The Acorns Early card is issued by Community Federal Savings Bank, member FDIC, pursuant to license by Mastercard International. Free trial for new subscribers only. Charges apply: $5+/mo after trial. Cardholder Terms and limits apply.