Hello to all of our new subscribers! If you found us from our recent edition of Home Economics, please note that we also send a weekly newsletter on Fridays delving into a newsier money topic, from how AI is affecting the white-collar workforce to an explainer on Trump accounts. Today’s Weekly Roundup isn’t exactly cheery, but we hope you like it! And if you want to submit your own Home Ec, you can do so here.

Last Saturday, I woke up to the scary news that the U.S. was at war with Iran. Though the Trump administration had been edging up to the attacks for months, I actually gasped when I checked my phone and saw the many notifications alerting me to the events of the night before.

That was just the beginning of the onslaught of news headlines that have caused me to feel true anxiety and despair in the days since. “Strike on girls’ school kills at least 175,” reads one. “The Iran war could rock the global economy,” reads another. Prediction market users are betting on the odds of nuclear war within the year. Gas prices are expected to spike.

And beyond the war, there’s plenty of other financial news to feel apprehensive about. A record high share of Americans are taking emergency hardship withdrawals from their 401(k)s, firms are laying off thousands of workers (and promising to let go of thousands more), and the cracks are beginning to show in private credit, which Wall Street has been trying to sell to retail investors for the past few years, and which the Trump administration just allowed in 401(k)s.

It has felt strange to go about my days writing about budgeting and splitting finances with my husband with all of this going on in the background. It’s a tension inherent to working in media that I’ve never been able to fully square. Every day, world-altering events take place, but, aside from deep worry about the state of things, my world is (thankfully) left more or less intact.

And while so much of the news feels bad, the truth is that there’s plenty of economic news to feel okay about. The stock market—at least before this week—keeps hitting record highs, and unemployment is still, somehow, relatively low (though rising). Trump administration officials assure us we’re doing better than ever. It’s hard to make sense of all of the conflicting and crazy-making news.

“The potential for whiplash is pretty high every single day,” Kevin Gordon, head of macro research and strategy at the Schwab Center for Financial Research, told Bloomberg.

Still, it seems like we’re all waiting, anxiously, for the other shoe to drop: for our employer to be the next to make widespread cuts, for a health insurance bill we won’t be able to afford, or for that long-awaited recession to finally hit. Add war to the mix, not to mention the many stressors in our home country, and it’s no wonder the majority of us feel negatively about the economy. While corporations and a handful of already incredibly rich people siphon all of the AI-fueled wealth and opportunities, everyone else hopes they still have a job in six months.

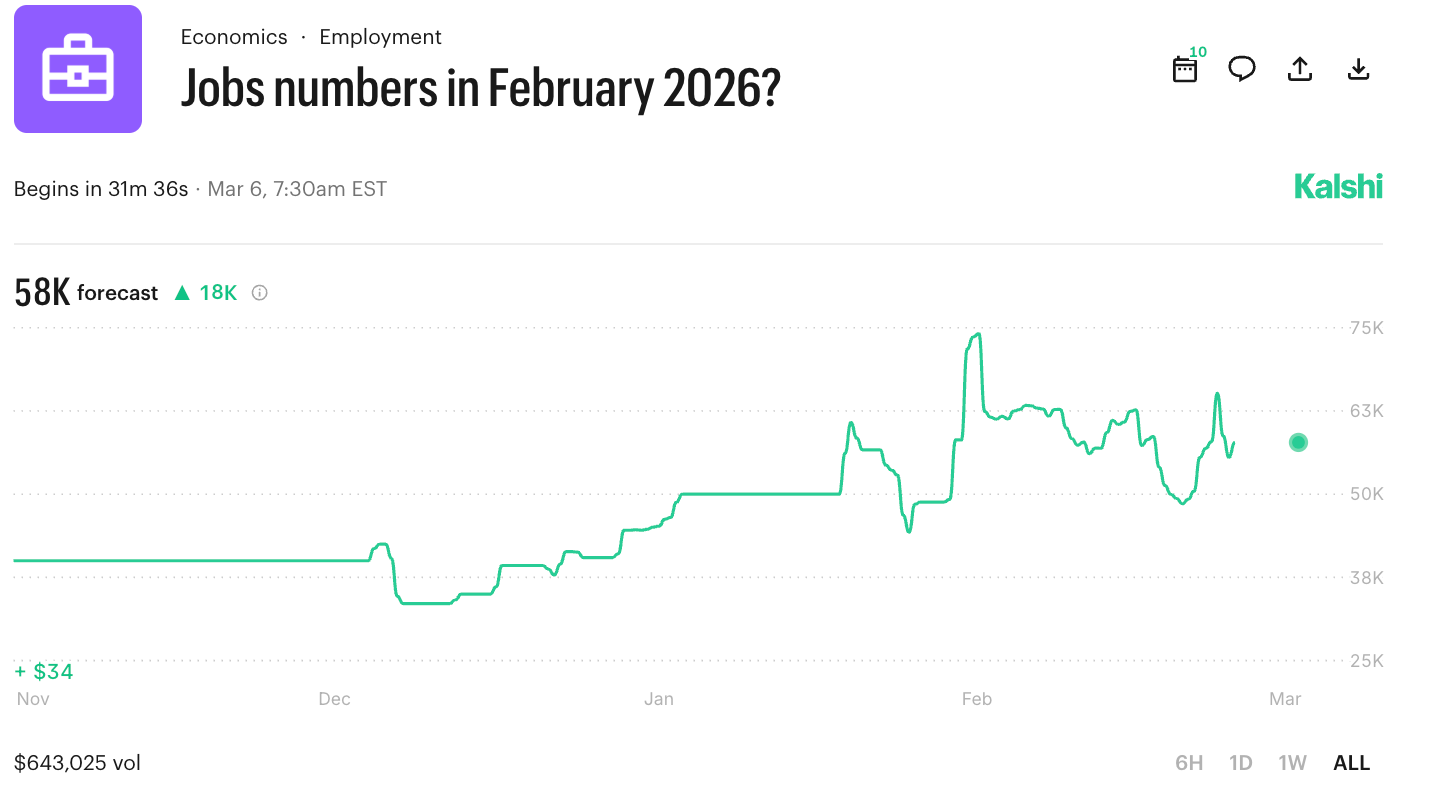

This all points to a sense that the overall economic system has transformed into something many of us don’t particularly enjoy living within. When the depravity economy seems to be growing day by day, the overwhelming feeling is that doing things the “right” way is no longer a viable path to a good life. You might not be able to afford groceries, but you can bet on last month’s jobs numbers, or on when U.S. forces will enter Iran in this unpopular, expensive war. Figure out a few ways to insider trade on Kalshi—which the platform says it doesn’t allow—and you might be able to make rent this month.

“Much of the American economy feels held together by cope and the gobs of money being thrown into AI, data centers, and gambling,” writes Jason Koebler of 404 Media. Even if the war ends tomorrow—which is less likely by the day, according to our president and the prediction markets—that sentiment wouldn’t change. Our troubles run, somehow, much deeper than that.

-Alicia

This weird economic moment in the news

- “Wars are never good for consumer sentiment,” Mark Brennan, an associate professor at New York University’s Stern School of Business, told CNBC. “They might be good for munitions, manufacturers and lobbyists and all these clowns, but not good for the average consumer.”

- I wrote about the U.S. casino economy and the many problems with financializing every aspect of everything a few months back, but it’s something I keep coming back to as we watch increasingly dystopian events play out each day.

- “Betting on geopolitics and military operations allows traders to profit off of death, and it transforms people, politics, death, trauma, everything into commodities,” writes Charlie Warzel in The Atlantic. “In the wake of the first strikes on Iran, Polymarket briefly allowed trades on when a nuclear weapon was likely to be detonated. Current events, no matter how heinous, become entertainment, a business plan, or both.”

- Speaking of which, bettors wagered $54 million on Ayatollah Ali Khamenei’s death. Now they’re not getting paid, The Washington Post reported.

- Trump keeps gambling with the economy—and getting away with it, writes Victoria Guida for Politico.

- So if the U.S. economy is doing so well, why aren’t we happier about it? “People don’t eat productivity or pay their rent with G.D.P.,” Jared Bernstein, a chairman of the Council of Economic Advisers under President Joe Biden, told The New York Times.

- Relatedly: The U.S. economy could be in a “boomcession.” (You knew we had to come up with a cutesy name for it.)

- NPR international correspondent Aya Batrawy is based in Dubai, and she spoke to her colleague Mary Louise Kelly about her experience living in the middle of a war zone. An Amazon data facility was bombed, and she’s been unable to do some normal, everyday things, like pay her phone bill, as a result.

- Friend of The Purse Matt Schulz wrote a helpful newsletter about what you should do with your personal money during these uncertain times, and Lindsey also recently wrote about how not to feel terrible about the news all of the time. (Perhaps harder to do this week!)

What else we’re talking about

- My friend Jen wrote this fascinating story about how Planned Parenthood is trying to make up for federal government budget cuts by offering services like Botox. -Alicia

- I’ve really enjoyed The Cut’s weeklong series “Seriously: Should I have a baby?” all about the complicated feelings that come with parenthood. I’m biased, as she’s an old friend and colleague, but I was especially moved by Andrea González-Ramírez’s piece, “Maybe Knowing Too Much About Motherhood Has Ruined Me.” ICYMI (and if you’re looking for a different perspective), I’m a big fan of motherhood! -Lindsey

- Are résumés on their way out? That’s what this Business Insider story posits. -Alicia

- We had a post go viral(ish) on Instagram, and it’s been an interesting experience! But also, just a reminder that we post lots of fun stuff over there, too, and if you’re not following us, please do!

On our radar

- It was great catching up with some of my favorite financial journalists at Northwestern Mutual’s annual Planning & Progress dinner this week! -Alicia (Lindsey is very jealous she missed it!)

- As I mentioned in February Receipts, I’m going to be in Austin next week for SXSW. I’m speaking on a panel hosted by Realtor.com, and it should be a good one! We’ll be talking about the rise of the female homebuyer at 2:30 p.m. on Saturday, March 14, at Realtor.com’s SXSW hub. The event is free, and you don’t need a badge to attend. You can register here. If you’re going to be in town for SXSW, let me know! I’m worried I’m going to end up bored and lonely like I was at FinCon! -Lindsey

TikTok of the week

@the_purse Let’s suppose these AI executives’ predictions come true, and most of the tasks performed as part of white-collar jobs are able to be automated in 12 to 18 months. If that’s the case…what’s the plan?

♬ original sound - the purse

Comment of the week

“Thank you for mentioning the importance of women having access to their own money!! Related to this, I think what a lot of people don’t spend time thinking about is how many women live within emotionally or physically abusive/controlling relationships and how controlling their money is a big part of that. I have a close person in my life who was trapped in an abusive relationship and had to walk away with literally nothing—all of her money was in accounts he controlled. She left with nothing and relied on friends and family to help her. That is so much harder to do once you have children. I say this because it’s a reality people don’t like talking about.”

-Crissy on Alicia’s story, “9 months into our marriage, I’m still Venmo-ing my husband for my half of the rent.” Join the convo!

Graph of the week

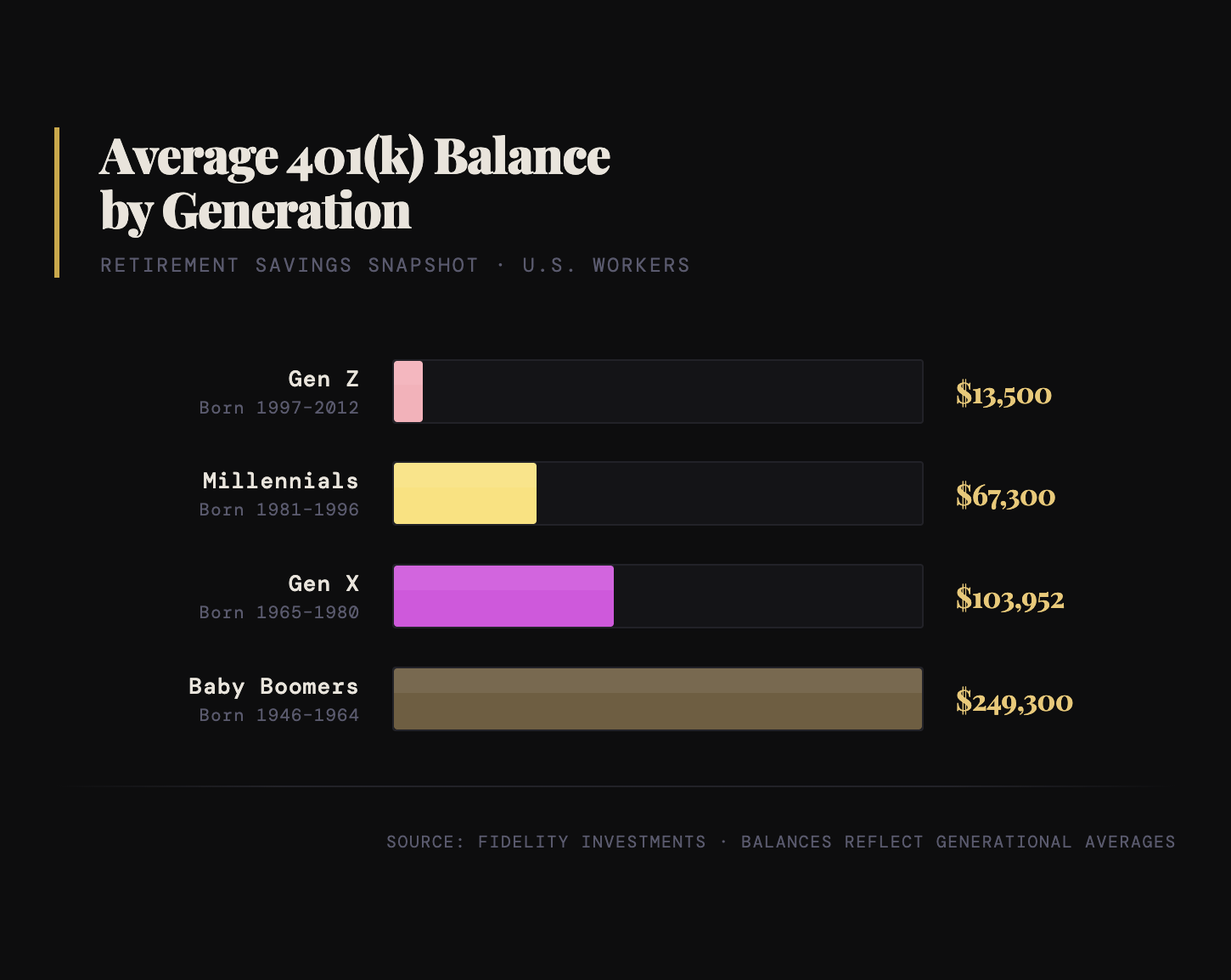

Some good financial news? Fidelity Investments reports that 401(k) balances were up more than 11% last quarter year-over-year. And 403(b) balances fared even better, with the average account increasing 13% in value over the previous year.

What else we published on The Purse this week

Lindsey's reflections on February + leaving Substack

Come chat about your February spending

Photos from our relaunch party last month

How Alicia and her husband are combining finances

Some info on a not-so-great trend

Best money we spent this week

- We got a lot of great comments on our post about clothes spending, so here’s where I admit I spent around $200 this week on new business casual clothing on Poshmark for an upcoming conference. Hopefully it looks good! -Alicia

- I had wayyyy too much to do last weekend, but instead of working all day Sunday, I decided to take my family ice skating. Sometimes, you just need a little fresh air and exercise to wash the anxiety away. I think it was $45 well spent, but I was a “mean mom” and wouldn’t also shell out for hot chocolate. -Lindsey